Open Review of Management, Banking and Finance

«They say things are happening at the border, but nobody knows which border» (Mark Strand)

Assessment of financial stability of banking systems

Abstract: The article studies the problems related to the assessment of the level of financial stability in the banking sector of the economy. It makes a strong case for the necessity and feasibility of using the Profit/Risk indicator (PR) for the assessment of the financial stability of commercial banks and the banking system.

The study is based on the analysis of methodological approaches to assessing financial stability in the banking sector, methods for assessing and aggregating banking risks used by international financial organizations and central banks. The study includes analysis of financial statements of commercial banks, provides time series with information on the level of financial stability and the magnitude of aggregated banking risks.

We propose a methodology for calculating the PR indicator, which allows quantifying the financial stability of both individual banks and banking systems. In this article, we propose a simplified method for estimating aggregate banking risks based on published financial statements of banks. We have also developed an assessment scale that allows producing a qualitative characteristic of the financial stability of both individual banks and the entire banking system. Based on the calculation of the profit/risk indicator (PR), we have analyzed the financial stability of the banking system of the Russian Federation for the 2016 – 2017 period. The article also features quantitative and qualitative assessment of financial stability, provides a comparative analysis of the financial stability of banks, grouped according to the institutional principle, and identifies and quantifies the dependence of the level of financial stability of the Russian banking system on its aggregate risks.

Using the methodology for assessing financial stability in the banking sector on the basis of the profit/risk ratio should enhance the quality of the created strategies for the development of banking systems, improve financial monitoring of the implementation of strategies, and focus the attention of banking supervisors on the detection of problems in the actions of banks at an early stage. The assessment of financial stability based on the PR indicator will be useful for minority shareholders and external users such as rating agencies, think tanks, and potential investors of banks.

Summary: 1. Introduction. – 2. The concept of financial stability. – 3. The different methodological approaches for the assessment of financial stability both from a quantitative and qualitative perspective. – 4. Conclusion.

1. The problem of ensuring the financial stability of banking systems has been gaining relevance recently. This is due to the fact that a weak banking system of any country can threaten the overall financial stability, both within the country and at the international level. In this regard, in the current circumstances, the most important task of central banks is to assess and monitor the financial stability of not only individual banks, but also national banking systems.

Shaping modern requirements to ensure financial stability in the banking sector of the economy, international financial organizations focus on improving the quality of banking risk management. In fact, according to the “Fundamental Principles of Effective Banking Supervision” [1] in order to maintain stability and confidence in the financial system, supervisors are encouraged to promote good corporate governance and maintain the proper level of the management of banking risks. At the same time, the effective banking supervision is aimed at individual banks, particularly at the individual and aggregated risks of these banks.

Today, central banks have accumulated extensive experience in assessing financial sustainability at the micro level, which relies on an analysis of the main banking risks. As for the assessment of financial stability at the level of banking systems in general, even its measurement poses certain challenges. This means that the assessment of financial stability of banking systems and measures to ensure it re-quire further improvement.

2. Analysis of scientific and specialized publications on this topic shows that the use of certain indicators of financial stability in studies of different levels is largely determined by the existing conceptual apparatus.

According to the classification proposed by G. Bårdsen, K. Lindquist and D. Tsomocos [2], there are two large groups of definitions of financial stability. The first group includes definitions based primarily on information characteristics. The second group includes institutionally-oriented definitions.

The authors believe that the first group includes the definitions of H. Minsky [3], F. Mishkin [4], O. Issing [5] and M. Foot [6]. The second group includes the works of A. Schwartz [7], E. Crockett [8], D. Tsomocos [9], A. Haldane [10], W. Allen and D. Wood (11), C. Gurhart and others. [12-16].

The first interpretation of the term “financial stability” is applied mainly to financial markets. Their increased volatility, as a rule, leads to the formation of so-called “bubbles” and thus negatively affects the economy. This opinion, in particular, is supported by Chant J. [17], Crockett A. [18], Ferguson R. [19,] Rosengren E.S. [20,], Kovalev M.M., Paseko S.I. [21], Stanik N.A. [22], Korolkov V.E., Yakushin A.P. [23].

In its second interpretation, the term “financial stability” is used as an analog of “financial sustainability”. On the one hand, this interpretation implies the ability of the financial system to withstand shocks that deteriorate the transformation of savings into investments and transfer of payments in the economy. This approach to financial stability is reflected in the work of Padoa-Schioppa T. [24], On the other hand, it implies a low level of systemic and individual risks within an object, the stability of which is investigated. This view is supported by Shinasi G. [25], Moiseev S.R., Lobanova M.A. [26], Lunyakov O.V. [27], Kadomtsev S.V., Israelyan M.A. [28]. In this case, the term “financial stability” applies to organizations, regions, financial (including banking) systems.

This approach is the basis for the analysis of financial stability conducted by the International Financial Institutions and Central Banks. For instance, the International Monetary Fund [29] in order to assess the financial stability, recommends using a list of indicators, including indicators of the sustainability of financial and non-financial corporations, household sector, financial market and real estate market. The Bank of Russia in the analysis of financial stability also uses indicators of the sustainability of financial and non-financial corporations, as well as financial markets [30, 31]. At the same time, state and supranational bodies regulating the banking system rely on the assessment of banking risks assumed by credit institutions in assessment of the financial stability of both individual banks and entire national banking system.

3. Methodological approaches to the assessment of financial stability on the basis of risks are explained in the works of a number of scholars. In fact, Bhattacharya S., Goodhart C.A.E., Tsomocos D.P., Vardoulakis A.P. [32] propose to conduct the assessment of the financial stability using an indicator defined as the difference between a safer and more risky asset portfolio per unit of borrowed funds. In the opinion of these authors, a shift in the structure of assets towards positions with a higher risk ratio against the increased borrowing will help trace the tendencies of decreasing financial stability.

Goodhart C. and Tsomocos D. [15, 16, 33] propose to assess the capacity of banks to assume risks on the basis of a combination of the probability of default of banks and their profitability. In this case, it is the combination of these two indicators that is important, since the increase in the probability of default itself can be a sign of an excessive risk taking, but will not necessarily cause a rise of the tension in the financial sector. A decline in the profitability of the banking sector itself could be a sign of a recession in the real economy, and not the increase in financial vulnerability. The existence of financial instability based on the principle of combining the probability of default and profitability, according to the authors of this approach, will be characterized by a simultaneous high probability of default and low profitability. In this case, the probability of default is associated with excessive risks. As the authors themselves believe, the advantage of this approach is that it can be applied both at the individual and at the aggregate level.

Other important concepts, associated with risk assessment, are the concepts of regulatory and economic capital. In accordance with Basel II [34], the regulatory capital is the amount of capital required by a credit institution to absorb its risks in accordance with the regulations established by the country’s regulatory authorities. Economic capital is notion similar to a regulative capital, but it is calculated not according to the regulator’s standards, but using some other methods. Essentially, these two indicators are quite close to each other. They show the value of own funds required by the credit institution to cover possible losses on risky assets and transactions. The ratio of equity capital to economic (or regulative) capital shows the level of reliability of a given organization. The higher this ratio, the higher the sustainability, i.e. the lower the risk.

The disadvantage of indicators in the concepts of regulatory and economic capital is the lack of a clear methodology for assessing the initial risks generated by banks. The indicator of regulatory capital is based on the methods used by regulators, and they are very simplistic and do not take into account many important factors. The indicator of economic capital implies the use of non-standard methods and renders incomparable results. The need for a significant amount of calculations creates difficulties when we try to apply these indicators to the banking system as a whole, rather than to an individual bank.

Another, much less obvious disadvantage of measuring risks through the minimum required capital is as follows. When determining these capitals, the event against which it is necessary to insure is the bankruptcy of the organization. The risk of bankruptcy consists of risks for individual assets and transactions in non-additive manner. First, the dependence here is more complicated; second, there is a strong influence of the correlation of risky events. For example, issued loans generate not only credit risk, but also the liquidity risk. Credit risk is important for the long-term sustainability of a bank. Liquidity risk is more important than credit in the short term. In the Russian banking system, most of the banking license revocations were triggered by liquidity problems, which were manifested in the depletion of money on correspondent accounts, delays in carrying out non-cash payments and return of deposits to customers. At the same time, banks with problems with loan portfolios, but with acceptable liquidity, continued to operate.

Another well-known idea is the calculation of the ratio of the bank’s profit to economic (or regulative) capital. It allows evaluating the performance of the credit organization in terms of possible investments in it. Taking into account that the number in the denominator is proportional to the magnitude of the risk, this ratio is, essentially, analogous to the profit/ risk ratio (PR). The ratio of profitability to risk shows the availability of sources of funds to cover risks, not only for banks, but also for the whole banking system. This allows using this indicator to assess its sustainability.

Thus, in many cases, the ratio of a certain value indicator to the size of the risks taken is used to assess the bank’s reliability. At the same time, the most difficult task is the assessment of risks. Assessment of the indicator in the numerator, whether it is the accounting capital, income, or something else, is very simple. Of all the options, the most favorable is the profit/risk ratio. This is a very common indicator used in investment analysis. However, it is not applied to banks because of the complexity of calculating the magnitude of bank risks. Thus, the practical use of the indicator (PR) for banks is reduced to solving the problem of assessing the risks of the bank.

Solving the problems of determining and identifying risks, the international financial organizations in their recommendations propose to assess the following main types of banking risks: credit risk, market risk, liquidity risk, operational risk, legal and reputational risks. At the same time, international financial organizations pay special attention to risk aggregation and reporting on risks [35].

Central banks develop their own methods for assessing the risks of credit institutions. Such methods, on the one hand, comply with the recommendations of international financial organizations, and, on the other hand, take into account the national peculiarities of banking systems. For example, the Bank of Russia uses its own methodology for assessing the financial stability of credit institutions, which includes the assessment of the following risks: credit, market and operational, strategic, and liquidity risk. To calculate individual risks, the Central Bank of the Russian Federation applies its own very simplified methods, which are available in public domain. To aggregate risks for assessing the sustainability of banks, the Bank of Russia uses the Scorecard approach [on methods for assessing the financial sustainability of a bank in order to recognize it as adequate to participate in the deposit insurance system see the Instruction of the Bank of Russia of June 11, 2014 N 3277-U; on assessing the economic situation of banks see the instruction of the Bank of Russia of April 30, 2008 N 2005-U]. For the calculation of mandatory standards, the additive method described in instruction 139-I is used [on the mandatory standards of banks see the instruction of the Bank of Russia N 139-I of December 3, 2012]. The application of the Scorecard approach is difficult due to the fact that the raw data are not available in the public domain. Risk assessment according to the instruction 139-I does not require access to data. The results of the 139-I risk assessment are published in their final form, because they are used in the calculation of the capital adequacy ratio H1.0. This most important standard of the bank is published monthly in the form of Report No. 135 “Information on mandatory standards and other performance indicators of the credit institution.”

In accordance with the instruction 139-I, the standard H1.0 should be calculated using the formula:

Н1.0 = C / (CR+MR+OR), (1)

where:

C is the amount of the bank’s equity funds (capital)

CR is the amount of credit risk,

MR is the amount of market risk,

OR is the amount of operational risk.

In a more general form, formula (1) can be represented as follows:

H1.0 = C / R, (2)

where:

R is the amount of the total risk assumed by the bank.

R can be found using formula (2):

R = C / H1.0, (3)

The amount of capital (C) can be found in the Report No. 123 “Calculation of equity funds (capital) (“Basel III”).” This indicator is updated once a month. Value of the standard H1.0. can be found in the Report No. 135, which is also updated monthly. It should be noted that the correctness of the calculation of all indicators of Report No. 123 and Report No. 135 is under the close supervision of the Bank of Russia, since the capital adequacy ratio is the most important standard for banks. Sometimes, the Report No. 135 can feature the risk value R itself, so that it can be used directly. In Reports No. 123 and No. 135, all data are given as of a certain date. In this regard, in order to calculate the index for a period, for example, for 1 month, it is necessary to average these data.

The aggregate amount of risks (R) obtained as a result of calculations according to formulas (1-3) can be used to determine the PR indicator using the formula:

PR = 12 P / R, (4)

where:

P is the profitability of the bank;

R is the amount of the total risk assumed by the bank.

We suggest using the amount of the current profit of the bank before tax as an indicator of the profitability of the bank. Profit data is available in Report No. 102 “Statement of financial results”, which is updated quarterly. Monthly profit in the simplest case can be found by dividing the quarter profit by 3. This will be sufficient for retrospective analysis, plotting, etc.

Multiplication by 12 is necessary to scale the indicator to yearly value, since the monthly profit is very small compared to the value of the total risk (R).

The PR ratio for the banking system can be calculated as the weighted average of the PR indicators for banks in the banking system. In this case, depending on the indicator used to weigh individual indices, two options are possible.

For the first option, we suggest using the value of bank assets as weights. In this case, the formula for calculating the index of financial stability of the banking system will look as follows:

, (5)

, (5)

where:

PRi is the individual financial stability index of the i-th bank,

Ai is the assets of the i-th bank,

A is the total assets of the banking system,

N is the number of banks.

For the second option, we can use the size of risks assumed by banks as weights. In this case, the formula for calculating the index of financial stability of the banking system will look as follows:

, (6)

, (6)

where:

PRi is the individual financial stability index of the i-th bank,

Ri is the value of the cumulative risk of the i-th bank,

R is the amount of cumulative risk of the banking system,

N is the number of banks.

In the second option, essentially, the formula (6) will be identical to the equation:

, (7)

, (7)

where:

PBS is the profit of the banking system;

RBS is the total risk of the banking system.

The choice of the calculation option is not essential for assessing the level of financial stability. The calculation results for both options will differ insignificantly. When using formula (6) for calculating the PR ratio, the PR values will be somewhat smaller than when using formula (5). This is due to the fact that the size of the risk assets of commercial banks is always less than the value of their total assets. However, this distinction must be taken into account in qualitative characteristics of the level of financial stability.

The values of the PR obtained from the formulas (1-6) do not allow giving a qualitative characteristic of the financial stability of the banking system. In order to solve this problem, we propose to use an evaluation scale that allows determining the level of financial stability by the actual values of the indicators. The scale has five options of qualitative characteristics of financial stability (table. 1).

As can be seen from Table.1, the levels of financial stability depend on the criteria corresponding to the values n1-n5. The proposed criteria should be formed based on the analysis of the financial stability of the banking system over a number of years, performed using the PR indicator. Naturally, for each national banking system the criteria for the formation of ranges will be different. So for the banking system of the Russian Federation based on the results of our analysis, we have formed ranges of financial stability with a step equal to 1.2% (Table.2). For calculating the PR indicator, we used the formula for weighing individual indices by asset level (5). In this case, the spread of data between their minimum and maximum values was taken into account. In the case of using in the calculation of PR formula (6), the boundaries of all ranges, with the exception of the lowest one, should be reduced by 3 points.

The step size 1.2% was chosen based on the following considerations. According to the banks’ financial reports, average term of loans in the banking system is approximately 3 years. The average amount of provisions for possible losses on loans is 9.4% average (including 10.3% for individuals) [Aggregated accounts for all Russian banks http://www.kuap.ru/banks/9999/balances/%5D. Assuming that future loan losses are approximately equal to the amount of reserves created, we find that banks will lose about 9.4% / 3 = 3.13% per year of the amount of loans issued. The profit of banks, used to calculate the PR indicator, has already been adjusted for this amount of created reserves. Therefore, if PR = 0, then it means that the bank’s revenues are barely enough to create reserves. If PR = 3.2%, then the bank can create reserves in double size. If PR = 6.4% in three times, etc. Since the possibility of double renewal alone greatly reduces the risk of bank failure, we took a value of 3.6% (with a small margin) as a criterion for high stability and divided the interval from 0% to 3.6% into three equal intervals.

Table 1

Rating Scale

| Assessment of financial stability | Index of Financial Stability (IFS) |

| High | n3< PR |

| Good | n3³ PR >n2 |

| Satisfactory | n2³ PR >n1 |

| Questionable | n1³ PR >0% |

| Low | PR £ 0% |

Table 2

Rating Scale for Russia

| Assessment of financial stability | Index of Financial Stability (IFS) |

| High | 3.6%< PR |

| Good | 3.6%³ PR >2.4% |

| Satisfactory | 2.4%³ PR >1.2% |

| Questionable | 1.2%³ PR >0% |

| Low | PR £ 0% |

Based on the proposed formulas (1-6) using the evaluation scale (Table 2) we performed the analysis of the financial stability of the Russian Federation for the period from January 2016 to June 2017. We have analyzed the largest banks of the Russian Federation, which were selected from the list of Top-30 as of July 1, 2017. The selection was made taking into account the availability of official financial statements of banks for the analyzed period on the Bank of Russia website [information on credit organizations is available at the Bank of Russia website. URL: http://www.cbr.ru/credit/%5D. As a result of the selection, 26 commercial banks were included in the sample, including 10 banks with state participation in the equity capital, 4 banks with foreign capital participation, and 11 banks from “other” category of banks. The share of assets of all analyzed banks in the total assets of the banking system as of April 01, 2017 was 76% of the assets of the entire banking system. General information on the analyzed banks is shown in Table.3.

Table 3

List of analyzed banks, ranked by the assets as of April 01, 2017

| Share in banking system assets | Type of ownership | ||

| 1. | SBERBANK OF RUSSIA | 0.270 | with state participation |

| 2. | BM-BANK | 0.117 | with state participation |

| 3. | VTB 24 | 0.066 | with state participation |

| 4. | VTB | 0.038 | with state participation |

| 5. | CREDIT BANK OF MOSCOW | 0.034 | other |

| 6. | ROSBANK | 0.034 | with foreign capital |

| 7. | BANK “OTKRITIE” | 0.033 | other |

| 8. | ALFA-BANK | 0.027 | other |

| 9. | GAZPROMBANK | 0.016 | with state participation |

| 10. | NATIONAL CLEARING CENTRE BANK | 0.015 | with state participation |

| 11. | UNICREDIT BANK | 0.015 | with state participation |

| 12. | BINBANK | 0.014 | other |

| 13. | PROMSVYAZBANK | 0.010 | other |

| 14. | ROSSEKLHOZBANK | 0.010 | with state participation |

| 15. | RAIFFEISEN BANK | 0.009 | with foreign capital |

| 16. | ROSSIYA BANK | 0.007 | other |

| 17. | SOVCOMBANK | 0.007 | other |

| 18. | SAINT-PETERSBURG BANK | 0.007 | other |

| 19. | CITIBANK | 0.006 | with foreign capital |

| 20. | AK BARS | 0.005 | with state participation |

| 21. | URAL BANK FOR RECONSTRUCTION AND DEVELOPMENT | 0.005 | other |

| 22 | JSCB “RUSSIAN CAPITAL” | 0.004 | with state participation |

| 23 | RUSSIAN REGIONAL DEVELOPMENT BANK (VBRR) | 0.004 | with state participation |

| 24. | NORTHERN SEA ROUTE (SMP-BANK) | 0.004 | other |

| 25. | YUGRA BANK | 0.003 | other |

| 26. | ORIENT EXPRESS BANK | 0.003 | other |

| Total | 0.763 |

Table 4 features the results of a quantitative and qualitative assessment of the financial stability of the banking system of the Russian Federation for the period from January 2016 to June 2017, obtained using the formula (5).

Analysis of the data in the Table 4 shows that in 2016 there was a gradual improvement in the financial stability of the banking system. PR at the end of 2016 increased 3 times compared with the beginning of 2016. This allowed the banking system in the Q4 2016 to improve its score from “questionable” to “good”. In Q1 2017, financial stability indicators deteriorated and financial stability once again returned to the “questionable” rating. However, compared with Q1 2016, financial stability proved to be almost 2.25 times higher, which indicates the stability of the trend of increasing financial stability.

Table 4

Assessment of financial stability of the banking system of Russia

For the period from 01.2016 to 06.2017

| Period | PR | Financial stability |

| January 2016 | 1.101 | Questionable |

| February 2016 | 1.102 | Questionable |

| March 2016 | 1.144 | Questionable |

| April 2016 | 1.895 | Satisfactory |

| May 2016 | 1.841 | Satisfactory |

| June 2016 | 1.801 | Satisfactory |

| July 2016 | 1.700 | Satisfactory |

| August 2016 | 1.691 | Satisfactory |

| September 2016 | 1.737 | Satisfactory |

| October 2016 | 3.016 | Good |

| November 2016 | 2.879 | Good |

| December 2016 | 2.876 | Good |

| January 2017 | 2.200 | Satisfactory |

| February 2017 | 2.177 | Satisfactory |

| March 2017 | 2.190 | Satisfactory |

| April 2017 | 2.433 | Good |

| May 2017 | 2.416 | Good |

| June 2017 | 2.415 | Good |

Fig. 1 shows the graphs describing the dynamics of the PR indicator of banks grouped by the type of ownership: banks with state participation (state banks), banks with foreign capital participation (foreign banks), and “other” banks.

Fig. 1. Dynamics of PR indicators of banks,

Grouped by the type of ownership

Fig. 1 shows that throughout the analyzed period only the financial stability of banks with state participation has changed in the same ranges as the overall indicator across the entire banking system. This is explained by the high proportion of banks with state participation in the assets of all banks analyzed (in January 2016 – 81%, in June 2017 – 79%). The financial stability of banks with foreign participation was characterized by low volatility, but in this regard, the stability level of these banks for the entire 15-month period was characterized by a “questionable” financial stability rating. The peculiarity of PR dynamics of “other” banks was in its high volatility relative to the general level and stability level of other banks. High volatility of financial stability of “other” banks was caused by the following reasons:

- The presence of losses in these banks in Q1 2016,

- Sharp improvement in financial results in Q4 2016.

The improved financial results in Q4 2016 were significantly influenced by such banks as:

- BINBANK (the monthly profit in Q4 was more than 4 bln. rubles against the losses in Q3 2016. The main factor of profit growth was the merger with MDM Bank);

- PROMSVYAZBANK (the monthly profit in Q4 was more than 3.5 bln. rubles against the losses in Q3 2016);

- ALFABANK (the monthly profit in Q4 was more than 7.8 bln. rubles against the losses in Q3 2016);

- AK BARS almost doubled its profits.

Due to a sharp improvement in financial results, “other” banks in October 2016 managed to enter a new, higher level of financial stability with a “good” financial stability rating. However, the month after, this stability rating returned to the level of “satisfactory”, and then (in Q4 2016) – to the “questionable”.

Fig. 2 presents graphs of financial stability indicators of the Russian banking system (PR1) and (PR2) and growth rates of risk assets (R) [the growth rate against the previous month, multiplied by 100] of the banking system for the 2016 – 2017 period. The index (PR1) was calculated using the formula (5), and PR2 – using the formula (6).

Fig. 2. The dynamics of the values of PR1 and PR2 and monthly increase

of the total risk (R, % per month) of the banking system of Russia

It can be seen from the graph that PR1 and PR2 change in a similar way. Therefore, it does not matter for the investigation of the dynamics, which of the indices to use. However, it is important for the ratings on the criteria scale. In future studies, we are going to use PR1.

Comparison of the dynamics of PR1, PR2 with the dynamics of growth in the total risk of the banking system of the Russian Federation allows to see the presence of a positive trend in all three indicators. Consequently, the correlation between the indicators is likely to be positive. At the same time, it follows from formula (4) that the correlation between PR and the level of risk (R) should be negative. Let us analyze this contradiction in more detail.

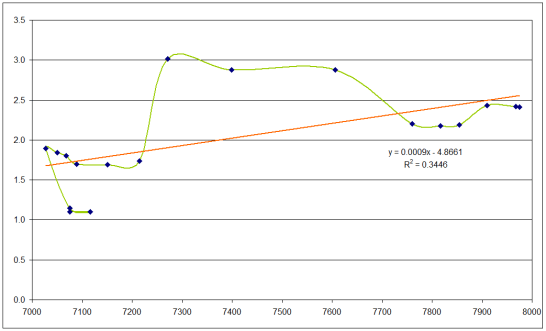

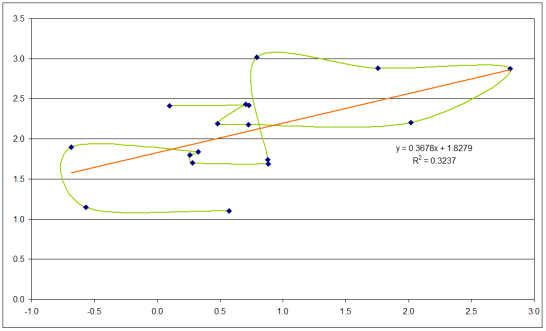

Fig. 3 and 4 show the dependence of PR1 on the magnitude of the risk (Fig. 3) and on the rate of risk growth (Fig. 4).

Fig. 3. Correlation of PR1

and the total risk (R, in bln. roubles) in the banking system of Russia

Fig. 4. Correlation of PR1 and

the growth rate of the total risk (R) in the banking system of Russia

As can be seen from the regression equations shown in Fig. 3 and Fig. 4, the correlation in both cases is positive: 0.587 for Fig. 3 and 0.569 for Fig. 4 respectively. There is a moderate positive correlation. It is explained by the fact that the profits of banks increased slightly more than risks. This is most likely due to the sampling of data, as the increase in the size of risk assets should not necessarily be accompanied by a faster growth in profits.

4. In general, the results of the analysis show that the proposed methodology for assessing financial stability on the basis of the ratio of profitability to risk has the following advantages:

- It allows giving both quantitative and qualitative assessment of financial stability in the banking sector of the economy, both at the micro- and macroeconomic level.

- The methodology is based on official reports that are publicly available and can be used for external evaluation of the level of financial stability by any interested party.

- In view of the regular publication of the initial statistical data, the proposed methodology ensures monitoring of financial stability with the same frequency and regularity.

- If the methodology is adapted to the financial statements of commercial banks of different countries, it can be successfully used to assess the financial stability of their banking systems and conduct cross-country comparative analysis.

- Using the proposed methodology, as well as the correlation dependence of the ratio of PR on the amount of accounted risks, the central banks will be able to quantify the strategic goal for the financial stability of the banking system, and to exercise timely control over its achievement.

- The assessment of financial stability based on the PR indicator can be used by banking supervisors to detect problems in the activity of banks at an early stage.

- The results of the financial stability assessment based on the PR ratio will be useful to minority shareholders and external users in the form of rating agencies, analytical centers, as well as frequent investors planning to place their savings in commercial banks.

References

- Core Principles for Effective Banking Supervision. Basel Committee on Banking Supervision, September 1997.

- Bardsen G., Lindquist K. G. and Tsomocos D. P. Evaluation of Macroeconomic Models for Financial Stability Analysis // Journal of World Economic Review, 2008, vol. 3, no. 1, pp. 7–32.

- 3. Minsky H.P. The financial instability hypothesis: a restatement // Thames Papers on Political Economy,

- 4. Mishkin F.S. Global Financial Instability: Framework, Events, Issues // Journal of Economic Perspectives, 1999, 13, no. 4, pp. 3–20.

- 5. Issing O. Monetary and financial stability: is there a trade-off? // Bank for International Settlements Papers, 2003, 18, pp. 16–23.

- 6. Foot M. Protecting Financial Stability — How good are we at it? // Speech at the University of Birmingham, 2003, 6.

- 7. Schwartz A.J. Real and pseudo-financial crises // Financial crises and the world banking system, Palgrave Macmillan UK, 1986, 11–40.

- 8. Crockett A. The theory and practice of financial stability // De Economist, 1996, vol. 144, no. 4, 531–568.

- 9. Tsomocos D.P. Equilibrium Analysis, Banking, and Financial Instability // Journal of Mathematical Economics, 2003, vol. 39, no. 5, pp. 619–655.

- 10. Haldane A., Hall S., Saporta V. and Tanaka M. Financial stability and macroeconomic models // Bank of England Financial Stability Review, 2004, 80–88.

- 11. Allen W.A., Wood G. Defining and achieving financial stability // Journal of Financial Stability, 2006, 2, no. 2, pp. 152–172.

- Goodhart C. A. E. Some New Directions for Financial Stability? // Bank of International Settlements, 2004.

- Goodhart C.A.E., Sunirand P., Tsomocos D.P. A Model to Analyse Financial Fragility: Applications // Journal of Financial Stability, 2004, vol. 1, pp. 1–35.

- Goodhart C.A.E., Sunirand P., Tsomocos D.P. A Risk Assessment Model for Banks // Annals of Finance, 2005, vol. 1, pp. 197–224.

- Goodhart C.A.E., Sunirand P., Tsomocos D.P. A Model to Analyse Financial Fragility //Economic Theory, 2006, vol. 27, pp. 107–142.

- Goodhart C.A.E., Sunirand P., Tsomocos D.P. A Time Series Analysis of Financial Fragility in the UK Banking System // Annals of Finance, 2006, vol. 2, pp. 1–21.

- Chant J. Financial Stability as a Policy Goal // Essays on Financial Stability, Bank of Canada Technical Report № 95, September 2003. P. 1–24. URL: http://www.bankofcanada.ca/ en/res/tr/2003/tr95.pdf .

- Crockett A. The Theory and Practice of Financial Stability. GEI Newsletter Issue № 6 (United Kingdom: Gonville and Caius College Cambridge), 1997, 11–12 July. URL: http://www.cepr.org/gei/6rep2.htm

- Ferguson R. Should Financial Stability Be an Explicit Central Bank Objective? Paper presented to an International Monetary Fund conference on Challenges to Central Banking from Globalized Financial Markets, 2002, September 17,. Washington, D. C., URL: http://www.federalreserve.gov/boarddocs/speeches/2002/20021016/default.htm

- Rosengren E.S. Definition of financial stability and some political consequences of application of the definition // Foreign researchers on the global financial crisis and its lessons, 2012, Moscow, INION, pp. 117-128. (In Russ.)

- Kovalev M.M., Paseko S.I. Providing financial stability – a new function of the state // Problems in management, 2013, no. 1 (46), pp. 20-33. (In Russ.)

- Stanik N. A. Bubbles are different: soap, financial and explosive // Financial analytics: problems and solutions, 2012,no 44 (134), pp. 38-46. (In Russ.)

- Корольков В.Е., Якушин А.П. Risk assessment and analysis of monetary policy in the context of large volatility of the stock market // In Situ, 2015, no 3 (3). pp. 46-50. (In Russ.)

- Padoa-Schioppa T. Central banks and financial stability: exploring the land in between // The Transformation of the European Financial System, 2003, pp. 269-310/

- Shinasi G. Defining Financial Stability // IMF Working Paper, October 2004, URL: http://www.imf.org/external/pubs/ft/wp/2004/wp04187.pdf.

- Moiseev S. R., Lobanova M. A. The concept of macroprudential policy // Money and credit, 2013, no 7, pp. 46-54. (In Russ.)

- Lunyakov O.V. Intercountry factor analysis of imbalances and the stability of the financial sector of the economy. Business Inform, 2013, no. 6, pp. 95-99. (In Russ.)

- Kadomtseva S.V., Israelyan M. A. Macroprudential regulation and development of an early warning system about potential occurrence of financial instability in Russia. Scientific Research of the Faculty of Economics. Electronic journal, 2015, vol. 7, issue 4, pp. 7-27. (In Russ.)

- Financial stability indicators. Guidelines for compiling.IMF, 2007, Washington D.C. (In Russ.) URL: http://www.imf.org/external/pubs/ft/fsi/guide/2006/pdf/rus/guide.pdf.

- Review of the international financial regulation system. Bank of Russia, July 2014, Moscow. (In Russ.)

- Review of financial stability. Information and analytical materials. Bank of Russia 2016, no. 2, Moscow. (In Russ.)

- Bhattacharya S., Goodhart C. A. E., Tsomocos D. P. and Vardoulakis A. P. A Reconsideration of Minsky’s Financial Instability Hypothesis //Journal of Money, Credit and Banking, 2015, vol. 47, no. 5, pp. 931–973.

- Aspachs O., Goodhart C.A.E., Tsomocos D.P. and Zicchino L. Towards a measure of financial fragility // Annals of Finance, 2007, vol. 3, pp. 37–74.

- Basel II: International Convergence of Capital Measurement and Capital Standards: a Revised Framework. Basel Committee on Banking Supervision, June 2004. URL: http://www.bis.org/publ/bcbs107.htm

- Principles for effective risk data aggregation and risk reporting. Basel Committee on Banking Supervision, January 2013, URL: http://www.bis.org/publ/bcbs239.pdf

Authors

Galina Gospodarchuk is Doctor of economics and Professor of the Department of Finance and Credit Lobachevsky State University of Nizhni Novgorod (e-mail: gospodarchukgg@iee.unn.ru).

Sergey Gospodarchuk is PhD in economics and individual researcher (e-mail: sergeyg1@yandex.ru).

You must be logged in to post a comment.