Open Review of Management, Banking and Finance

«They say things are happening at the border, but nobody knows which border» (Mark Strand)

“Size & fit” of piecemeal liquidation processes. Aggravating circumstances and side effects.

by Rosa Cocozza and Rainer Masera

Abstract: This paper investigates the actual impact of new accounting and regulatory requirements on banks’ provisioning policies and earnings management in the context of the capital adequacy of Euro Area (EA) credit institutions. This paper also examines whether loan-loss provisions signal managements’ expectations concerning future bank profits to investors. Evidence drawn from the 2011-2019 period indicates that earnings management is an important determinant of LLPs for EA intermediaries. During recent years, small bank managers are much more concerned with their credit portfolio quality and do not use LLPs for discretionary purposes apart from income smoothing. The paper gives evidence of a lack of flexibility in the Balance-Sheet of smaller banks and provides some policy refinement to avoid disorderly piecemeal liquidation.

JEL codes: G01, G21, G28, M41

Sommario

1. Introduction. – 2. A depiction of the main trends. – 3. Lights and Shadows of LLPs determinants. – 4. Literature review. – 5. Empirical analysis: data and model specification. – 6. Conclusions. – 7. References.

1. Introduction

The concept of proportionality, embedded in all legal systems, aims at keeping the level of public intervention – in the form of rules and restrictions or sanctions – appropriate to what is actually needed to achieve the desired social objectives. In banking regulation, proportionality should ensure that rules are applied in a manner that is appropriate, considering the bank’s size and internal organization and the nature, scope and complexity of its activities. The drivers for proportionality are not only the size of banks, but also their business models, complexity, and systemic relevance. In theory, simple and “easy to apply rules” are necessary for small and medium-sized banks, while more sophisticated banks may develop their own systems, tailor-made for the risks of their business and their groups.

Therefore, proportionality is originally a matter of calibration of prudential requirements: the existence of resilient business models should not be put at risk by excessively high requirements or by requirements which are not relevant for some business models. Eventually, proportionality turns into a matter of “costs”. Complex approaches are costly to implement, and they may have no added value when it comes to measure the risk incurred by simple activities. In addition, undue complexity is another source of risk for both banks and regulators. Thus, banks with a simple and limited activity should be able to implement simplified approaches to avoid undue complexity. In this perspective, proportionality, boosting calibrated diversity, contributes to the resilience of the banking sector. Or else, at least, it should.

Ultimately, proportionality poses a question of adequacy of interlocutors and not merely of instruments or procedures. The adequacy regards both the supervisory approaches and the actor’s characteristics. As a matter of fact, there is the need for an inner consistency in the financial system, guaranteeing a level playing field for the industry and creating reciprocity between protagonists and antagonists as well as between supervised entities and supervisors, thus giving rise to the concept of “regulatory adequacy framework” (Cocozza, 2019).

The banking crisis discipline cannot be secluded from this framework. Or, once again, at least it should not. Focusing on the crisis management framework for banks, within the European Union legal framework, the resolution procedure can only be used when public interest is at stake. It appears that resolution is available for a small number of large banks. Other banks’ crises must be handled through national insolvency procedures. As known, national insolvency regimes normally result in a piecemeal liquidation, which gives no guarantees that exit from the market will take place in an orderly fashion. If interested acquirers cannot be rapidly identified, liquidation will lead to theimmediate disruption of the bank’s core activities, to the disposal of assets and collateral at fire sale prices, and to non-insured creditors having a lengthy wait to obtain partial and uncertain reimbursement. Confidence in other banks may be shaken, with possible knock-on effects on the real economy. A disorderly piecemeal liquidation process is clearly not efficient and entails serious concerns, given the social and economic importance of the banking industry. A solution has thus to be found to avoid disorderly piecemeal liquidations for banks, as has been recognized by many authorities and commentators.

Hence, there is a growing concern about the possibility of direct losses arising from mis-marked complex instruments as well as about the implications that disorderly piecemeal liquidation process can have on reputation, and perceived ability to control the business, and about a huge scatter of prospective profit margin originated by banks, because of fire sale prices in case of unduly managed liquidation.

Solutions to avoid disorderly piecemeal liquidation for banks can assume many potential shapes from a policymaker perspective. Nevertheless, solutions must consider coeval conditions that could require a (fine?) tuning of intervention to avoid vicious spillover. Procyclicality is one of the main issues related to the regulatory framework which imposes capital requirements to be calculated as a percentage of bank risky loans: it entails that supervisory capital requirements are higher when economic conditions get worse, and lower in case of economic upturn. Procyclicality is generally considered a sort of acceptable side effect, at least if the context is not extremely severe. On the contrary, if the situation turns to be dangerous, procyclicality could end up “the” risk driver, since capital requirements could become paradoxically “lethal requirements”. This is today issue for many reasons. Inter alia, three are the major concerns.

Firstly, the COVID-19 pandemic is inflicting high and rising human costs worldwide, and the necessary protection measures are severely impacting economic activity. As a result of the pandemic, according to the International Monetary Fund (IMF, 2020b) the global growth is projected at –4.9 percent in 2020, 1,9 percentage points below the April 2020 World Economic Outlook (WEO) forecast. The COVID-19 pandemic has had a more negative impact on activity in the first half of 2020 than anticipated, and the recovery is projected to be more gradual than previously forecast. In 2021 global growth is projected at 5.4 percent. Overall, this would leave 2021 GDP some 6½ percentage points lower than in the pre-COVID-19 projections of January 2020. The adverse impact on low-income households is particularly acute, imperiling the significant progress made in reducing extreme poverty in the world since the 1990s. The risks for even more severe outcomes, however, are substantial. Effective policies are essential to forestall the possibility of worse outcomes, and the necessary measures to reduce contagion and protect lives are an important investment in long-term human and economic health. Because the economic fallout is acute in specific sectors, the IMF recognizes that policymakers will need to implement substantial targeted fiscal, monetary, and financial market measures to support affected households and businesses domestically. Growth in the advanced economy group – where several economies are experiencing widespread outbreaks and deploying containment measures – is projected at -6,1 percent in 2020. Most economies in the group are forecast to contract this year, including the United States (-5,9 percent), Japan (-5,2 percent), the United Kingdom (-6,5 percent), Germany (-7,0 percent), France (-7,2 percent), Italy (-9,1 percent), and Spain (-8,0 percent). In parts of Europe, the outbreak has been as severe as in China’s Hubei province (IMF, 2020a). Although essential to contain the virus, lockdowns and restrictions on mobility are extracting a sizable toll on economic activity. Adverse confidence effects are likely to further weigh on economic prospects. In a nutshell, from the banking perspective, credit risk is growing at faster pace than ever.

Apart from the economic downturn, there are two main aggravating circumstances to be considered extremely relevant: the so called “calendar provisioning” and the actual implementation of IFRS9. As part of the prudential framework, the Addendum of the ECB (ECB, 2018) raise the supervisory expectations about prudential provisioning, by imposing a predetermined time horizon for the total impairment of those exposures that are classified – or reclassified from performing to – non-performing, in line with the European Banking Authority’s definition, after 1 April 2018, irrespective of their classification at any moment prior to that date, implementing to the so called “calendar provisioning”. As a matter of fact, within 2 (7) years of NPE vintage for unsecured (secured) loan, the impairment process has to be terminated.

Moreover, the implementation of the IFRS9 for the accounting periods beginning on or after 1 January 2018. The International Financial Reporting Standards came into effect in January 2005 for the European Union banks. These market-oriented standards are supposed to increase financial disclosure and the overall reliability of financial reporting, if compared to the local generally accepted accounting principles. Furthermore, since they admit a limited number of options and do not allow hidden reserves, their application should make less likely the discretionary use of Loan Loss Provision (LLP) by bank managers (Barth et al., 2008; Leventis et al., 2011). According to the IFRS/IAS 39, loan assessment is based on the amortized cost and LLPs are calculated on the so called “incurred loss”, i.e., a loss already occurred or presumed on the basis of an event already occurred, though after the loan was granted. The adoption of a more forward-looking approach to loan-loss provisioning, based on the “expected credit loss” contributes to the additional exacerbation of growing credit risk impact, especially if, as in our case, the definition/identification of Non-Performing Exposure (NPE) is strictly set by regulators.

Therefore, the economic downturn might be coupled with procyclical effect of contemporary bank capital adequacy regulation and accounting principles[1] and might have significant impact on banks of different size. Among the extreme consequences, we could list “a sort of credit crunch” due to diseconomies of regulation because of procyclicality of capital adequacy, especially in the form of Loan Loss Provisions (LLPs), as well as a fatal impact on different banks with various business model because of the increasing spur – in terms also of moral suasion – towards the reduction of Impaired Loan ratio (IL) “whatever it takes”.

The final target of the study is, therefore, the evaluation of the procyclicality and of the implementation of the IFRS9 on the provisioning policies across banks of different sizes, to evaluate the relative importance of these aggravating circumstances.

The remainder of the paper is organized as follows. In section 2, we briefly summarize the current main trend as from the European Central Bank Supervisory Statistics. Section 3 provides a literature review, developing the rationale for managers to use their discretion in estimating loan-loss provisions. Section 4 describes the data, the sample selection process, and the methodology we adopt in our analysis. In section 5 we present and discuss the empirical evidence. Section 6 concludes the discussion also with policy implication.

2. A depiction of the main trends

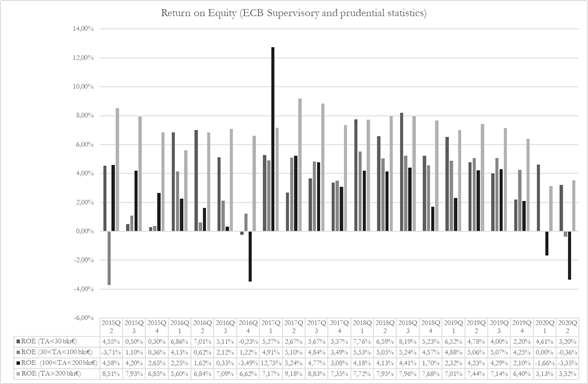

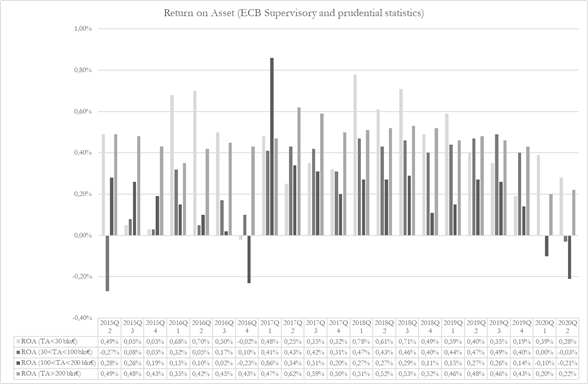

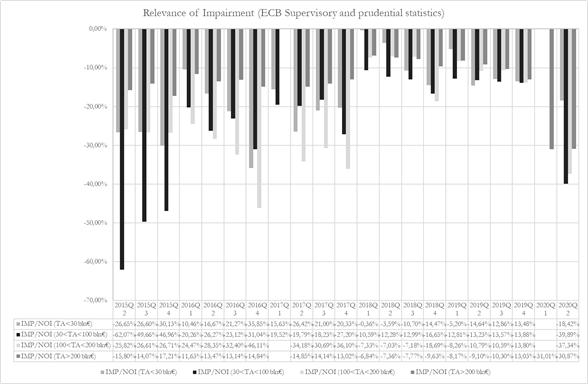

An insight into the most recent (2015-2020) dynamics of key performance indicators such as Return On Equity (ROE), Return on Asset (ROA) and Cost/Income Ratio (CIR) returns an image of the main current trends in profitability and solvability. According to the ECB Supervisory and prudential statistics[2], the average reducing ROE and ROA exhibit a more relevant shrinkage for medium-large and large banks rather than for medium-small and small institutions whereas the CIR grows more rapidly for small and medium-large banks rather than for the others (Chart 1, Chart 2, Chart 3, Chart 4). The incidence of the impairment (IMP) on the Net Operating Income boosted in the first month of the current year.

If we concentrate on the standard deviation of the series, we observe a noteworthy difference in the variability of the returns, accounting for assorted risk exposure, which appears more relevant for medium-large banks (Table 1).

Table 1

As a matter of fact, small banks show more stable figures than medium ones with reference to ROE. Unsurprisingly, large banks are less risky and more capable to control costs, and therefore efficient, according to modern portfolio theory. The resulting allocation of smaller banks under the efficient frontier or, in other words, their meager profitability normally raises question about the overall sustainability of certain business models and ends up encouraging merger and consolidation, as the most effective ways to achieve economies of scale and decrease relative costs. However, banks are aware of the potential hidden consequences of these operations – for example, loss of local focus (particularly when mergers entail the closing of local branches) or risks stemming from the integration of different IT systems. In addition, the cost of performing due diligence on target banks is a considerable side effects of acquisitions.

Chart 1

Chart 2

Chart 3

Chart 4

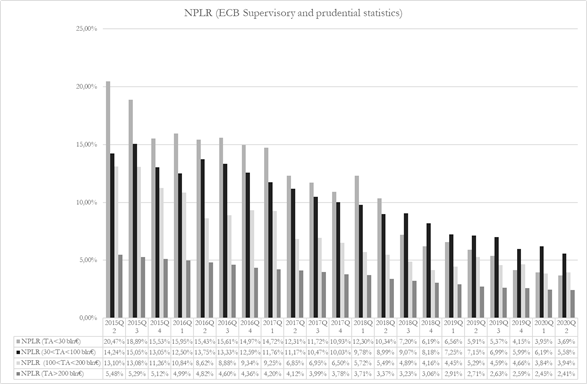

One area of main attention is the asset quality, both for capital requirements and substantial business development. According to the best practice, banks should adopt a formalized strategy for optimizing Non-Performing Loan (NPL) management by maximizing the current value of recoveries. This strategy should be defined based on an analysis of their management capabilities, the external environment, and the characteristics of their non-performing portfolios. It must strike the best possible balance between the various recovery options: internal workout solutions or outsourcing to credit collection specialists; forbearance; foreclosure; legal procedures or out-of-court negotiations; disposals (including securitization transactions) with accounting and prudential derecognition of the assets sold. As a matter of fact, banks have recently devoted their efforts – “whatever it takes” – towards the reduction of NPL, as shown by Chart 5 and Chart 6 depicting both the NPL ratio (NPLR) and the Coverage Ratio (CR).

Table 2

| CR | NPLR | SR | |||||||

| Mean | St. Dev. | Slope | Mean | St. Dev. | Slope | Mean | St. Dev. | Slope | |

| TA<30bln€ | 41,63% | 2,48% | 0,33% | 11,06% | 5,18% | -0,82% | 20,04% | 1,16% | 0,02% |

| 30<TA<100bln€ | 43,35% | 1,85% | 0,20% | 10,15% | 2,96% | -0,47% | 18,36% | 1,55% | 0,17% |

| 100<TA<200bln€ | 44,00% | 2,53% | 0,15% | 7,22% | 3,00% | -0,46% | 18,30% | 0,52% | 0,07% |

| TA>200bln€ | 43,53% | 1,23% | -0,16% | 3,80% | 1,00% | -0,16% | 18,16% | 1,36% | 0,19% |

Chart 5

Chart 6

Chart 7

Chart 8

Chart 9

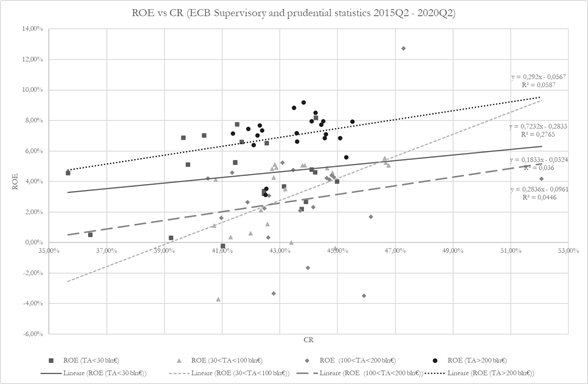

It is also worth mentioning that the drop in the NPLR have dissimilar impacts on the ROE of diverse size banks. As shown by Chart 7, larger banks report a decline in ROE alongside the reduction of NPLR whilst smaller bank face the opposite. This poses a fundamental question on the real economic impact of the NPL cutback, mainly if it is pursued by selling “whatever it takes”. The inverse correlation between the ROE and the NPLR detected for small and medium small banks (Chart 7) could imply that the NPL increase –– forces smaller bank to raise provisioning and reduce, ceteris paribus, profit margin. In other words, we could face a situation in which even more often “the operation was successful, but the patient died”. At the same time, the inverse correlation between ROE and NPLR could account for a business model merely focused on credit supply and, therefore, unable to recover loan loss and provision with other income areas. This could reinforce the belief that larger banks, thanks to a intermediation portfolio less focused on lending, are able to counterbalance the increase in loan loss and provision with other sources of profit, mainly connected to services (commission and fees)[3].

Besides, the prevailing positive relationship between ROE and CR (Chart 8) confirms that bank equity acts as income propeller, providing buffer margin for increasing costs and additional expenses. This role is far sharper in small banks (see slope figure in Chart 8) than in the others, since they show the highest average solvency ratio (SR) over the reported years (Chart 9 and Table 2).

Therefore, we observe a growing stiffness of the balance-sheet architecture for smaller banks. The statement’s anelasticity, due to a limited diversification of the business model and to the supervisor’s imperative towards NPE reduction, makes smaller banks less capable to react promptly to economic shocks. The COVID-19 pandemic is not only a sudden shock, but a “persisting downturn” and it might be enhanced in its hazardous effect by procyclicality in the capital requirement and prudential provisioning, creating a favorable environment for disorderly piecemeal liquidation.

3. Lights and Shadows of LLPs determinants

As known, loan-loss provisions (LLPs) are one of the main accrual expenses for banks. The role they play within a bank’s financial statements is crucial, given the sensitive information they convey: LLPs are set aside to face a future deterioration of credit portfolio quality. However, provisioning policy can pursue goals that are different from a fair representation of the evolution of a bank’s loan losses. Prior research suggests four central reasons to explain managerial behavior concerning LLPs: income smoothing, capital regulation, signaling, and taxes. The main purpose of this study is, therefore, to examine the use of loan-loss provisions in managing earnings and regulatory capital ratios and in signaling managers’ private information concerning a bank’s future earnings within the European banking industry as an aggravating circumstances of the piecemeal liquidation processes.

Papers addressing the issue of LLP’s as a key variable in depicting the future bank outcomes detect the potential changes in banks’ behavior in earnings and capital management via LLPs. With reference to European banks, Fonseca and Gonzàlez (2008) study the institutional factors affecting income smoothing via LLPs in banks globally, including a number of European countries, finding that income smoothing is negatively related to: investor protection, accounting disclosure, restrictions on bank activities, and external and internal supervision. Bouvatier and Lepetit (2008) report that poorly capitalized European banks are constrained to expand credit and that loan-loss provisions are made to cover expected future loan losses, intensifying credit fluctuations. On the contrary, LLPs used for management objectives do not affect credit fluctuations. Perez et al. (2006) test the use of loan-loss provisions for income smoothing and capital management within the Spanish banking system, finding evidence that supports income smoothing but not capital management. By examining a sample of 91 listed European banks, Leventis et al.(2011) find that earnings management is significantly reduced after the implementation of the International Financial Reporting Standards (IFRS) and that capital management is not significant in both pre and post IFRS regime. Using a sample of 491 banks over the period 1996-2006, and comparing banks from Euro Area (EA) countries and banks from countries where the Euro currency is not used, Curcio and Hasan (2013) find that: loan-loss provisions reflect changes in the expected quality of banks’ loan portfolio; earnings management is strongly supported for EA but not for non-EA banks; non-EA institutions do use loan-loss provisions to signal private information to outsiders, whereas EA banks do not; and, finally, restrictions on bank activities and stronger creditors protection help to reduce incentives to smooth earnings, especially in the EA banking systems. They also examine for a restricted sample of 195 banks, provisioning policies during the financial crisis. During the 2007-2010 time horizon, they find evidence of a change in banks’ behavior in terms of their use of loan-loss provisions at both EA and non-EA intermediaries. Particularly, loan-loss provisions become pro-cyclical and are not used to smooth bank income any more at EA credit institutions, whereas, contrary to what is observed during the 1996-2006 period, non-EA banks use LLPs as a tool for income smoothing during the crisis, but not for managing their capital ratios or to convey private information to the market.

Provisioning plays a crucial role in ensuring the safety and strength of banking systems and hence is a key focus of bankers and bank supervisors. Asset quality reviews (AQRs) and stress tests (STs) have further highlighted the need for consistent provisioning methodology and adequate provisioning levels across banks. Historically, accounting rules have pursued two alternative goals: the conservative valuation of assets, which is central in the European accounting system, and the accurate measurement of each period’s net income, strongly emphasized by the American accounting set of rules.

With reference to Non Performing Exposure (NPE), supervisors foster both adequate measurement of impairment provisions through sound and robust provisioning methodologies and timely recognition of loan losses within the context of relevant and applicable accounting standards (with a focus on IAS/IFRS accounting standards) and timely write-offs. At the same time, they promote enhanced procedures including significant improvement to the number and granularity of asset quality and credit risk control disclosures (ECB, 2017). The adequacy provisioning framework include the identification of individual or, as appropriate, collective assessment of impairment[4] and the estimate future cash flows. The estimate involves a fundamental reference to the appropriate accounting standard (IAS 39/IFRS9), since it lay down the principles for impairment recognition. IFRS 9 financial instruments, which replaced IAS 39 for the accounting periods beginning on or after 1 January 2018, require among other things the measurement of impairment loss provisions based on an expected credit loss (“ECL”) accounting model rather than on an incurred loss accounting model as under IAS 39, thus enhancing the anticipation of the actual losses and stressing procyclicality. Potentially, the above described set of rules represents a step forward in the direction of a higher level of accounting transparency. Nevertheless, the new accounting rules could made bank returns more volatile, and lending policies even more pro-cyclical than the past.

As stated, the Addendum of the ECB raise the supervisory expectations about prudential provisioning, by imposing a predetermined time horizon for the total impairment of those exposures that are classified – or reclassified from performing to – non-performing, in line with the European Banking Authority’s definition, after 1 April 2018, irrespective of their classification at any moment prior to that date, implementing to the so called “calendar provisioning”. According to the Addendum, unsecured NPEs must be totally impaired after 2 years of NPE vintage, while secured NPEs must be entirely impaired after 7 years of NPE vintage. Moreover, if the applicable accounting treatment is not considered prudent from a supervisory perspective, the accounting provisioning level is fully integrated in the banks’ supply to meet the supervisory expectation by means of all accounting provisions under the applicable accounting standard including potential newly booked provisions and by means of expected loss shortfalls for the respective exposures in default in accordance the CRR, and other Common Equity Tier 1 deductions from own funds related to these exposures. In any case, if the applicable accounting treatment does not match the prudential provisioning expectations, banks also have the possibility to adjust their CET 1 capital on their own initiative. In other words, under normal conditions, banks must fulfill supervisory expectations “whatever it takes”. That is why, calendar provisioning has been addressed as a “nuclear time bomb” if not somehow disarmed in the COVID-19 pandemic times.

Besides, bank provisioning policies can make a system of capital requirements procyclical, depending on what kind of losses capital requirements are designed to face. If it is the only unexpected loss, provisioning policies can reduce capital requirements’ procyclicality since banks would increase loan-loss provisions during good periods, with good profit margins, while they would draw from these reserves when the credit loss amount gets higher. If capital requirements are designed to cover also the expected loss, procyclicality stretches to the provisions as well. This is certainly stressed by the combined effect of IFRS9, calendar provisioning implementation and the very bleak expectations for economies[5].

4. Literature review

Several papers have dealt with bank managers’ incentives in using loan-loss provisions as a management tool. Here we examine the results of prior literature along the three main objectives pursued by bank managers via LLPs: regulatory capital management; earnings management practice, aiming at stabilizing bank net profit over time; and, finally, signaling the earnings that management thinks the bank will be able to obtain in the future.

The hypothesis of capital management via loan-loss provisions is based on the idea that bank managers use provisions to avoid the cost associated with the violation of capital adequacy requirements. Given the actual set of rules, an increase in loan-loss provisions has conflicting effects on Tier 1 and Tier 2 capital. On the one hand, higher LLPs diminish, via a reduction in retained earnings, Tier 1 capital; on the other, an increase in loan-loss provisions cause higher loan-loss reserves and, consequently, raise Tier 2 capital. Empirical results on the issue of the use by bank managers of this accounting accrual to manage regulatory capital ratios are not consistent, and are mainly focused on U.S. banks. Research by Ng et al. (2011) investigates the relationship between loan-loss reserves added back as regulatory capital and the risk of bank failure. Particularly, by focusing on the effect of the add-back of loan-loss reserves in 2007 on U.S. bank failures and other performance metrics during the three following years, they show that there is a positive association of these add-backs with bank failure, and that this relationship is especially concentrated for those banks that use add-backs to increase their regulatory capital, thus confirming the paradox that, in some cases, capital requirements might be “lethal”.

Using data prior to the period in which Basel I came into effect, some studies concluded that LLPs were a tool for managing regulatory capital (Scholes et al. (1990); Moyer (1990); Beatty et al. (1995); Kim and Kross (1998); Ahmed et al. (1999); Anandarajan et al. (2007)). In contrast with these results, investigating heterogeneity across banks’ capital-raising decisions, Collins et al. (1995) find a positive influence of capital on loan-loss provisions, meaning that when bank capital is low, managers tend to decrease loan-loss provisions rather than increase them, and they show that banks use write-offs more than loan-loss provisions to manage capital ratios. Among the others, Bouvatier and Lepetit (2008), investigating banks’ pro-cyclical behavior for a sample of 186 European banks, show that poorly capitalized banks use loan-loss provisions to manage regulatory capital. On the contrary, Leventis et al. (2011), focusing on 91 European listed banks, examine the impact of the implementation of IFRS on the use of LLPs to manage bank capital and find no support for the capital management hypothesis.

Earnings management implies the manipulation of reported earnings in such a way that the bottom line of the profit and loss account does represent a “specific” economic result of a bank’s activity. A specific kind of earnings management is income smoothing, aiming at reducing the variability of net profit over time. In order to stabilize net-profit, bank managers will increase (decrease) loan-loss provisions when earnings (before loan-loss provisions) are high (low). Income smoothing incentives can derive from a bank manager’s will to adjust a bank’s current performance to a firm-specific mean, as pointed out by Collins et al. (1995), or to the average performance of other benchmark-banks, as highlighted by Kanagaretnam et al. (2005). Furthermore, as to the reasons why managers smooth out a bank’s income, Bhat (1996) underscores that income smoothing improves the risk perception of a bank to regulators; it helps to stabilize, over time, managers’ compensation; it allows managers to grant a steady flow of dividends to bank stockholders; and it maintains bank stock price stable by reducing earnings volatility.

Literature related to industrial firm financial reporting has extensively investigated the income smoothing rationale (Barnea, Ronen and Sadan, 1975; Ronen and Sadan, 1981; Fudenberg and Tirole, 1995; Trueman and Titman, 1988; and Goel and Thakor, 2003), but addressing the banking literature allows us to add a perspective that industrial firms-related literature cannot assume. In fact, in banking, the issue could also be analyzed from the supervisory authority’s point of view. On the one hand, banks are required by regulators to set loan-loss provisions aside against expected credit losses; on the other hand, they have to raise an adequate amount of capital to face unexpected credit losses. In this view, regulators’ interest is in reducing bank pro-cyclical behavior: banks should increase loan-loss reserves during good times, and draw resources from these reserves when the economy slows down and potential defaults become real. As a consequence, bank earnings management might also be the result of a manager’s attempt to meet capital adequacy requirements.

There is a huge collection of banking literature, mainly U.S.-based, regarding the use of loan-loss provisions for income smoothing. This research provides mixed empirical results: Greenawalt and Sinkey (1988) find that regional banks are more likely to be involved in income smoothing than money-centered banks. In a study examining, among other issues, the influence of loan-loss provisions as a tool for earnings management, Ma (1988) shows that U.S. commercial banks used loan-loss provisions and charge-offs to smooth reported earnings. Surprisingly, he finds no relationship between loan portfolio quality and loan-loss provisions. His results indicate that bank management tends to raise (lower) bank loan-loss provisions in periods of high (low) operating income, thus using LLPs as a pure tool for earnings management. Collins et al. (1995) also find a positive relationship between earnings management and LLPs, thus supporting the notion that banks smooth income over time to a firm-specific mean. Bhat (1996) demonstrates that banks are more likely to be involved in income smoothing practices if they are small and in poor financial condition. More recently, Anandarajan et al. (2007) show that Australian commercial banks are engaged in earnings management practices, especially if they are publicly traded.

In contrast, some researches find conflicting evidence: Scheiner (1981), Wetmore and Brick (1994), Beatty et al. (1995), and Ahmed et al. (1999), among others, find no evidence of income smoothing. The latter study, in particular, does not find strong evidence of earnings management via LLPs after Basel I came into effect. This is somewhat surprising, as one would expect to see evidence of more aggressive earnings management since the new capital adequacy regulation removed the constraints associated with earnings management, if compared to the previous regulatory set of rules. Finally, investigating the cross-country determinants of income smoothing within a sample of banks from different countries, Fonseca and Gonzàlez (2008) find that the incentive to smooth earnings increases in more developed and market-oriented financial systems. Furthermore, according to their results, bank incentives to smooth income are lower in banking systems characterized by higher levels of accounting disclosure and official and/or private supervision, and by stricter restrictions on banking activities. Bouvatier and Lepetit’s (2008) evidence on a sample of European banks is not consistent with the income smoothing hypothesis: they find that banks reduce loan-loss provisions when earnings before taxes and loan-loss provisions increase, and this strengthens the cyclicality in loan-loss provisions due to the non-discretionary components since earnings are higher during periods of growth. Leventis et al. (2011) find a general support to the earnings management hypothesis, though this practice is significantly reduced after the implementation of IFRS in 2005.

Prior research documents a positive relationship between stock returns and loan-loss provisions, suggesting that the market could look at LLPs as a signal of bank managers’ private information about future earnings rather than as future credit losses. In particular, Beaver et al. (1989) find that, conditional on the reported level of non-performing loans, higher loan-loss allowances are associated with higher market-to-book ratios: in their view, loan-loss provisions can indicate that management perceives the earnings power of the bank to be sufficiently strong so that it can withstand additional provisions. Theory does not unambiguously support the signaling hypothesis.

Loan-loss provisions are made up of two parts: the first, discretionary or unexpected, is under managers’ control; the second, non-discretionary or expected, is related to physiological changes in default risk, due to the ordinary growth of loan portfolio. After controlling for unexpected changes in non-performing loans and unexpected charge-offs, Wahlen (1994) finds a positive association between discretionary provisions and both future cash flows and bank stock returns. This suggests that private investors can interpret increases in discretionary LLPs as good news and not as the anticipated deterioration of credit portfolios’ future quality; bank managers would try to convey to investors the signal that a bank’s future earning capacity can easily bear additional provisions. Liu and Ryan (1995) find that the market reaction to LLPs is positive for banks with a high percentage of large and frequently renegotiated loans, and that the advance market anticipation of LLPs is stronger for these banks. According to Liu et al. (1997), the market interprets higher discretionary loan-loss provisions as good news only if banks appear to experience default risk problems. Beaver and Engel (1996) observe that the valuation coefficients on the discretionary and non-discretionary components of LLPs are positive and negative, respectively, consistent with the signaling hypothesis. In contrast to the aforementioned papers, Ahmed et al. (1999) and Anandarajan et al. (2007) do not find any evidence of signaling behavior by the banks examined in their respective studies on U.S. and Australian banks. Finally, Bouvatier and Lepetit (2008) find evidence supporting the signaling hypothesis for the sample of European banks they analyze.

5. Empirical analysis: data and model specification

Data used in this study are from Bankfocus database, drawn from the period 2011 – 2019. The sample contains 1648 banks with at least three years of balance-sheet data and it is made up by 117 commercial banks, 1109 cooperative bank, 411 savings bank and 11 bank holding and holding company. From the sample, outliers were secluded by eliminating the extreme bank/year observations when a variable presents extreme values (bank specific variable less than 1% and higher than 99%). From a geographical perspective, all the banks belong to the most relevant countries within the Euro Area. The majority are from Germany, followed by Italy, France and Spain (Table 3)[6].

Table 3

To explain the dynamic of the LLPs we use a model able to verify the relevance of regulatory capital management, income smoothing, and signaling and procyclicality. The model is set as follows:

where:

LLP is the dependent variable and is the ratio of loan-loss provisions to total assets; GDPGR is the GDP growth rate;

IL is the ratio of non-performing loans to total assets;

GL is the ratio of customer loans to total assets;

EBTP is the ratio of earnings before taxes and loan-loss provisions to total assets;

TCR stands for total regulatory capital and takes the value of the total regulatory capital ratio minus 8 and divided by 8 when observations for bank i are in the first quartile and 0 otherwise;

SIGN is the one-year ahead change in earnings before taxes and loan-loss provisions as defined in Bouvatier and Lepetit (2008):

TA is the natural log of total assets.

This model is a modified version of the cross-sectional model used by Ahmed et al. (1999), Anandarajan et al. (2007), Leventis et al. (2011) and Curcio and Hasan (2013).

The variables chosen as predictors are traditionally used to test for procyclicality, income smoothing, capital management, and signaling. The dependent variable of our regression model is LLPi,t, the ratio of loan-loss provisions to total assets at time t for the bank i. Detecting whether bank managers use their discretion to manage capital and earnings would be easier if we had the opportunity to separate the discretionary component from the non-discretionary part of loan-loss provisions. Prior research proxied the non-discretionary component through variables representing the current level and the dynamics of losses within the loan portfolio (see, among others: Ahmed et al., 1999; Hasan and Wall, 2004; Anandarajan et al., 2007; Fonseca and Gonzàles, 2008; and Bouvatier and Lepetit, 2008). Hence, to control for the non-discretionary component, we use:

- ILi,t, the ratio of non-performing loans to total assets that occurred at the bank i at time t. In a loan-loss accounting system which distinguishes between general and specific provisions, non-performing loans can be considered a proxy for the specific component. Loan-loss provisions are expected to be positively related to changes in non-performing loans;

- GLi,t, the ratio of the amount of bank i total customer loans to its total assets at time t, which can be thought of as a proxy to capture general provisions. As stated by Lobo and Yang (2001), the influence of this variable on loan-loss provisions largely depends on the quality of incremental loans.

The inclusion of annual growth in the gross domestic product (GDPGR) at constant prices aims at controlling for the pro-cyclical effect of loan-loss provisions and captures the effect of macroeconomic conditions on loan-loss provisions (Laeven and Majnoni, 2003; Bikker and Metzemakers, 2005; Anandarajan et al., 2007; and Fonseca and Gonzàlez, 2008). We expect a negative coefficient because banks will increase loan-loss provisions the event of an economic downturn.

As to the discretionary factors, Ahmed et al. (1999), Moyer (1990), Beatty et al. (1995), and Leventis et al. (2011) all adopt the ratio of actual regulatory capital before loan-loss reserves to the minimum required regulatory capital to indicate the use of loan-loss provisions for capital management. We follow Curcio and Hasan (2013) and use the variable TCRi,t, which takes the value of the total regulatory capital ratio minus 8 and divided by 8 when observations for bank i are in the first quartile of the total capital ratio and 0 otherwise. If poorly capitalized banks are less willing to make loan-loss provisions in order to increase their regulatory capital endowment, we expect a positive correlation between LLPi,t and TCRi,t. Nevertheless, since loan-loss provisions are negatively correlated with Tier 1 capital, which includes equity and retained earnings, and positively with Tier 2 capital, we should underline that accounting relations could also influence the relation between bank capital and loan-loss provisions.

Based on the vast majority of prior literature – see, among others, Ahmed et al. (1999), Hasan and Wall (2004), Anandarajan et al. (2007), Bouvatier and Lepetit (2008), Fonseca and Gonzàles (2008), Leventis et al. (2011), Curcio and Hasan (2013) – in order to test for the income smoothing hypothesis, we consider the variable EBTPi,t, which is the ratio of earnings before taxes and loan-loss provisions to total assets for bank i at time t. This hypothesis is supported if its coefficient has a positive sign, meaning that banks with earnings lower (higher) than their target value tend to reduce (increase) loan-loss provisions to stabilize them.

To test the signaling hypothesis, we include the variable SIGNi,t, which is defined as the one-year ahead change in earnings before taxes and loan-loss provisions, as in Bouvatier and Lepetit (2008). Particularly, this variable can be expressed as follows: SIGNi,t = (EBTPi,t+1 − EBTPi,t )/0.5(TAi,t + TAi,t+1). The use of earnings before taxes and provisions to test for the signaling hypothesis can also be found in Ahmed et al. (1999) and Anandarajan et al. (2007). Since the signaling hypothesis states that discretionary changes in loan-loss provisions are positively correlated to future changes in future earnings, we expect a positive sign for the coefficient of this variable.

Size has been set taking as small banks those whose total asset are within the first quartile of the distribution of logarithm of total asset and as large those exceeding the fourth quartile. Medium banks are defined by difference (second and third quartile).

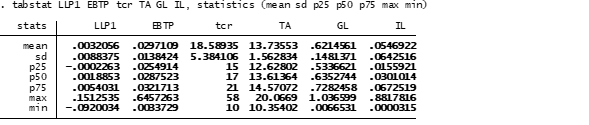

Tables 4-7 provide descriptive statistics for the period 2011-2019 for our sample banks. With regards to the credit quality of our sample banks, non-performing loans (IL) are, on average, 5,47% of total assets. As to the profitability of our sample banks, the ratio of earnings before taxes and loan-loss provisions to total assets (EBTP) is 2,97%. Both the variables, as well as the total capital ratio, are, as expected from §2, inversely correlated with bank size.

Table 4 All banks

Table 5 Small banks

Table 6 Medium banks

Table 7 Large banks

The empirical analysis aims at detecting whether different size banks behave differently in the use of loan-loss provisions as a tool for regulatory capital management, for income smoothing, and as a signal to the market, according to the hypotheses described in the previous section. Shedding more light on the existence of differences in provisioning practices is relevant from the banking authorities’ perspective, because higher accounting discretionary power can be an important competitive advantage for some banks relative to others and render ineffective the “leveling playing field” objective that international regulators pursue.

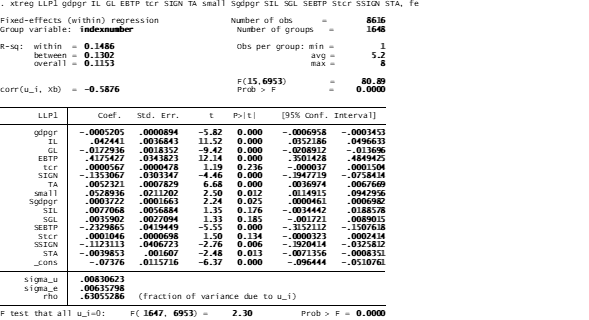

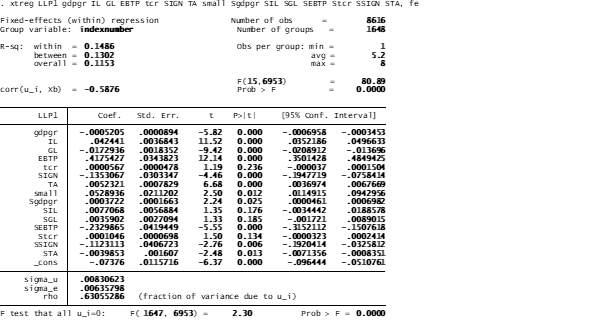

The basic model for the comparison is based on previous equation, which is estimated for the whole sample and separately for banks of different size, according to the TA classification stated in § 4. The model has been also estimated secluding the last two years (2018-2019) to evaluate the impact of the implementation of IFRS9.

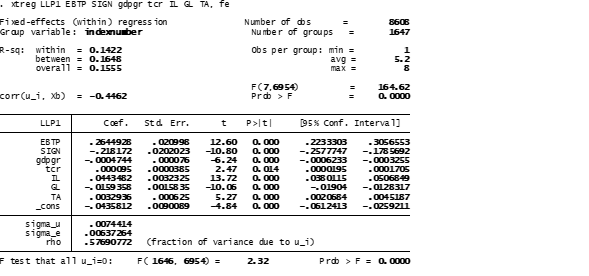

Table 8 All banks (2011-2019)

Table 9 All banks (2011-2017)

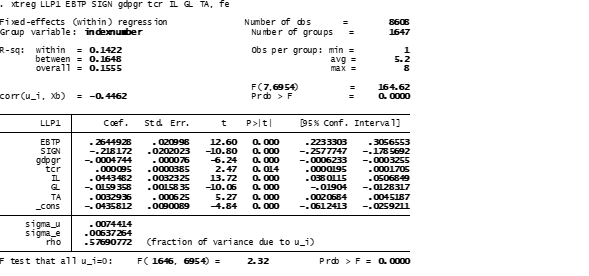

The results show that:

- the GDP growth rate (GDPR) is significantly associated with the ratio of loan-loss provisions to total assets for the whole sample. Consequently, we find evidence of banks’ pro-cyclical behavior: an economic downturn forces banks to increase LLPs. The rational for such a behavior can be traced back to the awareness that an economic downturn could result in higher credit risk exposure;

- the TCR in slightly significant for the LLPs dynamic. As stated, if poorly capitalized banks are less willing to make loan-loss provisions to increase regulatory capital endowment. The small figure of TCR coefficient might therefore be interpreted as limited discretionary in the definition of the LLPs;

- the EBTP is positively associated to the LLPs, thus giving raise to the income smoothing usage of LLPs, especially in “rainy day”;

- the variable SIGN is significant but negative. Therefore, discretionary in loan-loss provisions is correlated to changes in future earnings. Nevertheless, the decrease in the LLPs against EBTP increase might be interpreted either as the absence of the signaling hypothesis or as lack of discretionary in provisioning;

- the negative sign on the GL could represent an overall improvement in the credit lending process, probably mainly due to the general drive towards a reduction of NPE even from regulators;

- needless to say that LLPs are positively correlated with the impaired loan and increase in TA, thus accounting for a physiological growth in the credit risk according to the loan expansion.

Table 10 and 11 report values of coefficient for all regressions. The barred cell exhibit figures that are not statistically significant at 1% or at 5%.

Table 10: Full period (2011-2019)

| All | Small | Medium | Large | |

| Independent Variable | Coefficient | Coefficient | Coefficient | Coefficient |

| GDPR | -0,0004744 | -0,0002192 | -0,0003991 | -0,0007009 |

| TCR | 0,000095 | 0,000226 | 0,000094 | -0,000019 |

| EBTP | 0,2644928 | 0,1734691 | 0,6660653 | 0,1849566 |

| SIGN | -0,218172 | -0,2732727 | -0,0689422 | -0,0472744 |

| GL | -0,0159358 | -0,011315 | -0,0190391 | -0,0082053 |

| IL | 0,0443482 | 0,048902 | 0,0477276 | 0,0482731 |

| TA | 0,0032936 | 0,0028147 | 0,0096393 | 0,0037803 |

Table 11: Restricted period (2011-2017)

| All | Small | Medium | Large | |

| Independent Variable | Coefficient | Coefficient | Coefficient | Coefficient |

| GDPR | -0,0004354 | -0,0002052 | -0,0003056 | -0,0006301 |

| TCR | 0,0000938 | 0,0001916 | 0,000091 | -0,0000501 |

| EBTP | 0,2623675 | 0,1437928 | 0,7429283 | 0,1991897 |

| SIGN | -0,2158839 | -0,2640454 | -0,0386505 | -0,0135444 |

| GL | -0,0151309 | -0,007604 | -0,0191615 | -0,0074526 |

| IL | 0,0436339 | 0,0495342 | 0,0475869 | 0,0494596 |

| TA | 0,003454 | 0,0024995 | 0,0105656 | 0,0046948 |

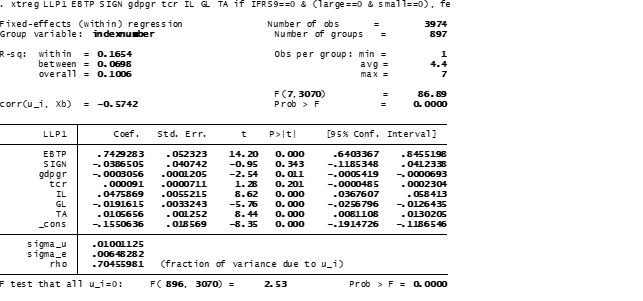

Table 12 Small banks 2011-2019

Table 13 Small banks 2011- 2017

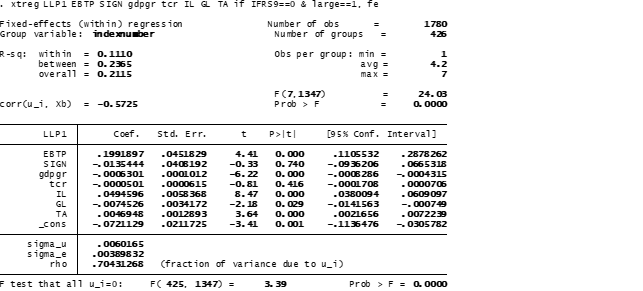

Table 14 Medium banks 2011 – 2019

Table 15 Medium banks 2011 – 2017

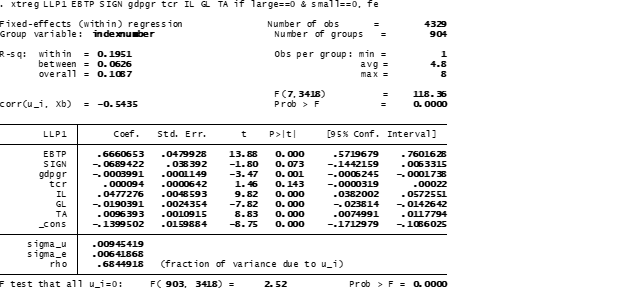

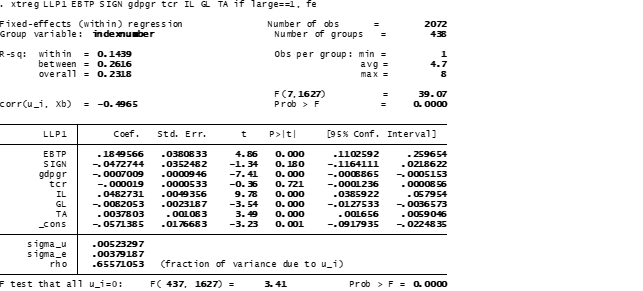

Table 16 Large banks 2011 – 2019

Table 17 Large banks 2011 – 2017

Results shows that the GDP growth rate (GDPR) is significantly associated with the ratio of loan-loss provisions to total assets for all the group intermediaries, except for small banks. Consequently, we do find evidence of banks’ pro-cyclical behavior, which is somehow unexpected for small banks because of the introduction of IFRS9, although the time length embraces just two years.

For all intermediaries, the coefficient of the ratio of non-performing loans to total assets (IL) is positive and significant. This is an expected result because it confirms the direct relation between LLPs and the considerable institutional and operational effort towards the reduction of the impact of credit risk. The estimated sensitivity of loan-loss provisions to the amount of customer loans is negative and significant even including the IFRS9 years. The negative sign of the coefficient does not confirm the prudent behavior by bank managers highlighted by Beaver and Engle (1996) in their paper on a sample of large U.S. banks. The average value of the coefficient on the IL does not show relevant value differences among groups, providing evidence of a stable contribution to LLPS. This implies that there is no proportionality in the provisioning process.

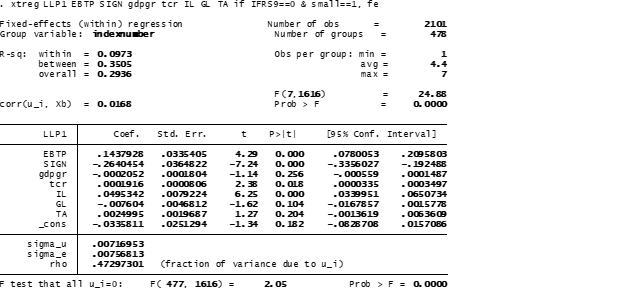

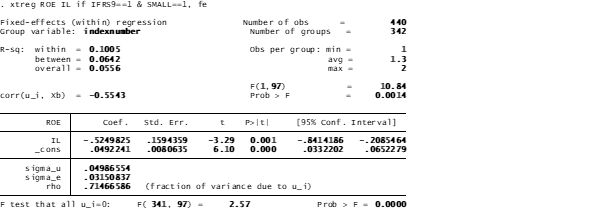

Although the analysis of the impact of the IFRS9 considers just two years, expected credit loss methodologies might intensify the adverse effect of the prospective negative economic cycle especially for small banks. A confirmation of the judgmental impact of the IFRS9 implementation can be gained by regressing the ROE on IL with IFRS (2011-2017) e without IFRS (2018-2019) (Table 19 and Table 20). As can be easily seen, the last years show a substantial increase in the negative relationship between the two variables, despite the overall improvement in the credit lending process.

Table 18 ROE and IL 2011-2017 (Small banks)

Table 19 ROE and IL 2018-2019 (Small banks)

As to the three hypotheses to be tested, the ratio of earnings before taxes and loan-loss provisions to total assets (EBTP) is positively associated with bank loan-loss provisions and is significant in all estimation, thus strongly supporting the income smoothing hypothesis. It is noteworthy that contribution of this independent variable is extremely relevant and shows significant difference across groups. For the whole sample, the EBTP contributes for more than ¼ of the LLPs variability and it does not show any significant figure distinction with the implementation of the IFRS9. Small banks and large appear to be less prone to income smoothing than medium banks where the coefficient provides for 2/3 and ¾ of the LLPs dynamics.

As to the signaling behavior, the coefficient of the variable SIGN is either negative or not significant. Consequently, our analysis does not support the signaling hypothesis concerning the use of loan-loss provisions as a tool to convey information about their future earnings to the market according to the prevailing literature. Nevertheless, the coefficient needs some attention because, as can be easily seen, where significant, it accounts for a relevant quota of the LLPs dynamics. On average for the whole sample the contribution is more the 1/5 and it is significant for small banks with some figure difference both with and without IFRS9 (Tables 10 and 11). This might be interpreted as a substantial tightness of the provisioning both for lack of discretionary and for stiffness of assessment arising from the NPE shrinkage. In this perspective, small banks appear to be no flexible as far as the provisioning is concerned.

Our evidence does not confirm the capital management hypothesis, since the coefficient of TCR is statistically significant only for small banks, thus entailing that these intermediaries can use only slightly LLPs to manage their capital ratios before the introduction of IFRS9.

Finally, coefficients on TA defined as the logarithm of the book value, , always positive, shows an extreme moderate impact of the business growth on the LLPs thus providing evidence of not sufficient diversification of portfolios since, as recently verified, costs of diversification outweigh its benefits, especially for large financial intermediaries (Ciocchetta, 2020), including global systemically important banks (G-SIBs). The coefficient is not significant for small banks, thus confirming once again the stiffness of the provisioning process with and without IFRS9.

Moreover, we add time dummy in the right side of the regression equation to control for different impact for small banks. Specifically, the “small” dummy takes the value of 1 for small banks, defined as stated as the first quartile of the TA distribution, and the null value for all the others. Table 18 presents the results of the estimation on the pooled sample to detect whether we find differences between small banks and the other institutions. The dummy variable “small” is positive and statistically significant, meaning that small banks are characterized by a significantly higher amount of loan-loss provisions to total assets if compared to other banks. This is consistent with the idea that small banks are devoting more resources to the impact mitigation of credit risk in order to reach the target level of exposure.

The interaction term S●GDPGR is statistically significant, entailing that small banks do not show the same of pro-cyclical behavior as others. Regarding the non-discretionary variables, we find that small banks’ provisioning decisions based on the amount of non-performing loans do not show differences statistically significant (the interaction term S●IL is not significant). The interaction term S●GL is positive but not statistically significant, entailing that the sensibility of small banks’ provisions to changes in the amount of the loan portfolio is equal to other banks.

As to our discretionary management hypotheses, we find evidence of different behavior between small banks and all the others regarding income smoothing, capital management and signaling. Particularly, the coefficient of the interaction term S●EBTP is negative and statistically significant. This provides further support to the difference already highlighted: small banks seem to be less prone to use LLPs to smooth their income. The interaction term S●TCR is characterized by a coefficient positive and statistically not significant, thus confirming the difference already pointed out about the capital management hypothesis. In any case, the effect is negligible given the small magnitude of the coefficient. The same evidence can be found for the signaling hypothesis, since S●SIGN is negative and significant at 1% confidence level, which means that, more than the rest of the sample, small banks do not use loan loss provisions to convey a signal about future earnings due to the burden of the current regulatory constraints on their provisioning policies. Small banks exhibit more rigidity in the balance sheet architecture.

Table 20 Small banks differential analysis 2011-2019

6. Conclusions

This paper reexamines earnings and capital management, and signaling explanations for the choice, by banks, of loan-loss provisions for a sample of 1684 banks from the main 4 Euro Area countries (Germany, France, Italy, and Spain) over the 9-year period 2011-2019, using data from the Bankfocus database. The paper also develops a comparison between these banks of different sizes in the overall provisioning policies. How banks account for impaired loans has a strategic impact on their reported earnings and capital and has been largely investigated by previous literature.

We investigate whether small banks behave differently relative to other institutions, since a deeper knowledge on provisioning practices can make more effective the supervisory objective of leveling the playing field from the regulators’ perspective.

Overall, we find evidence that: (i) loan-loss provisions reflect changes in the expected quality of banks’ loan portfolio, measured by the amount of non-performing loans; (ii) earnings management is an extremely important factor affecting provisioning decisions for banks; (iii) the desire to signal private information to outsiders does not explain provisioning policies for sample intermediaries. Though always linked to the credit portfolio quality, EA institutions’ LLPs appears to be pro-cyclical and are used to smooth income over time but not for managing their capital ratios or to convey private information to the market.

Besides, we found strong evidence of a considerable anelasticity of the provisioning in small banks, thus giving rise to a fundamental question on the effectiveness of “proportionality principle”. The detection of such effect forces us to explore the cause, since it can be traced back to both diseconomies of scale and regulatory diseconomies. This is our main future research prospect.

As far as the expected credit loss (ECL) methodologies are concerned, beyond the general point that IFRS 9 can become procyclical in a severe economic downturn, such as the current COVID-19, we find that there is a judgmental impact for small banks. ECL methodologies have long been promoted by the supervisory community for their potential to enhance the transparency of financial statements and improve the accuracy of reported loan values and associated expected credit losses. In addition, they require banks to provision earlier in the credit cycle, helping to mitigate the excessive procyclicality associated with the incurred loss model. This is certainly true in the prospect of a growing cycle. However, coping with a negative cycle, ECL methodologies could substantially aggravate the profitability for the “anticipation” of prospective losses. In the wake of the Covid-19 pandemic, there have been calls to either delay the application of ECL provisioning frameworks or to apply the standards with greater flexibility. These pleas are premised on the notion that banks should support the real economy in these unprecedented times, and that an overly conservative application of ECL provisioning in the current circumstances could lead to a spike in banks’ non-performing loans, thus increasing provisions, lowering earnings and pressuring regulatory capital. This, in turn, may affect the availability of credit to affected consumers and businesses (Zamil, 2020).

Research on the use of loan-loss provisions is meaningful for banking supervisors who will have to ensure that provisions cover expected losses, and that capital is used for unexpected losses. From a prudential point of view, the empirical evidence points out the need for a sound accounting framework. A natural extension to the analysis developed here is the consideration of a more in-depth study that takes account of specific factors and regulatory practices in individual countries. In this area an interesting future research prospect could be a comparison with the US (Masera 2019 and Petropoulou 2020), where One Size Fits All (OSFA) regulation has not be adopted and the ECL methodologies will be mandatory for most banks from 2023. A comparison between the two systems for the same time could offer an insight on some ad-hoc “exemptions” to ECL systems in case of steady economic downturn. More generally a comparison of banks performance on the two sides of the Atlantic should help avoid/contain the pitfalls of non ergodic stochastic systems and there attendant path dependence (Hicks 1980, Tsay 2010 and Peters 2019).

Further research should also attempt to provide evidence on the usefulness of the reform of LLPs, with particular attention to the impact of calendar provisioning, dramatically highlighted by the COVID-19 pandemic.

References

Abad, J. and Suarez, J., 2017, Assessing the cyclical implications of IFRS 9 – a recursive model, ESRB Occasional Paper Series No. 12.

Ahmed, A.S., Takeda, C., Thomas, S., 1999. Bank loan loss provisions: a reexamination of capital management, earnings management and signaling effects. Journal of Accounting and Economics 28, pp. 1-25.

Anandarajan, A., Hasan, I., McCarthy, C., 2007. Use of loan loss provisions for capital, earnings management and signaling by Australian banks. Accounting and Finance 47 (3), 357-379.

Barnea, A., Ronen, J., Sadan, S., 1975. The implementation of accounting objectives: an application to extraordinary items. Accounting Review 50, 58-68, January.

Barth M.E., Landsman W.R., Lang M.H., 2008. International accounting standards and accounting quality. Journal of Accounting Research 46, pp. 467-498.

Barth, J.R., Caprio, G.Jr., Levine, R., 2001. The regulation and supervision of banks around the world: A new database. World Bank Working Paper N. 2588.

Basel Committee on Banking Supervision, 1988. International Convergence of Capital Measurement and Capital Standards, Document N. 4, July.

Basel Committee on Banking Supervision, 2006. International Convergence of Capital Measurement and Capital Standards. A Revised Framework, June.

Basel Committee on Banking Supervision, 2009. Guiding principles for the revision of accounting standards for financial instruments issued by the Basel Committee, August.

Basel Committee on Banking Supervision, 2010. Basel III: A global regulatory framework for more resilient banks and banking systems, December.

Beatty, A., Chamberlain, S., Magliolo, J., 1995. Managing financial reports of commercial banks: The influence of taxes, regulatory capital, and earnings. Journal of Accounting Research 33, 2, 231-262.

Beaver, W., Eger, C., Ryan, S., Wolfson M., 1989. Financial reporting and the structure of bank share prices. Journal of Accounting Research 27, pp. 157-178.

Beaver, W., Engel, E., 1996. Discretionary behavior with respect to allowances for loan losses and the behavior of security prices. Journal of Accounting & Economics Vol. 22 (1-3), pp. 177-206.

Bhat, V., 1996. Banks and income smoothing: an empirical analysis. Applied Financial Economics 6, 505-510.

Bikker, J.A., Metzemakers, P.A.J., 2005. Banks provisioning behavior and procyclicality. Journal of International Finance Markets, Institutions and Money, 15, vol. 2, pp.141-157.

Bouvatier, V., Lepetit, L. 2008. Banks’ procyclical behavior: Does provisioning matter? Journal of International Financial Markets, Institutions & Money, 18, 513-526.

Boyd, J., Graham, S., Hewitt R., 1993. Bank holding company mergers with non-bank financial firms: effect of the risk of failure. Journal of Banking and Finance 17, 43-63.

Ciocchetta F., 2020. Asset diversification and banks’ market value. Notes on Financial Stability and Supervision, No. 20, 2020.

Cocozza R., 2018. Regulatory framework adequacy: quesiti aperti per le banche di dimensione non qualificata. Rivista Bancaria Minerva Bancaria, 4, 109-115.

Cocozza R., 2019. NPL: Lascia o raddoppia, Relazione presentata al convegno ‘‘La problematica dei crediti deteriorati. Rischi ed opportunità’’, Università Parthenope, Napoli, 18 ottobre 2019.

Cocozza R., 2020. Intermediazione creditizia e credito deteriorato: un binomio (im)possibile?, Studi in onore di Antonio Dell’Atti, a cura di S. Dell’Atti, Giuffré Francis Levfebre, 477- 494.

Collins, J., Shackelford, D., Wahlen, J., 1995. Bank differences in the coordination of regulatory capital, earnings and taxes. Journal of Accounting Research 33, 263-292.

Curcio D., Hasan I., 2013, Earnings and capital management and signaling: the use of loan-loss provisions by

European banks. The European Journal of Finance 21, 26-50.

Demirgüc-Kunt, A., Detragiache, E., 2002. Does deposit insurance increases banking system stability? An empirical investigation. Journal of Monetary Economics 49, 1373-1406.

European Central Bank, 2017, Guidance to banks on non-performing loans, Frankfurt.

European Central Bank, 2018, Addendum to the ECB Guidance to banks on nonperforming loans: supervisory expectations for prudential provisioning of non-performing exposures, Frankfurt.

European Central Bank, 2020a, Press Release. March 20. https://www.bankingsupervision.europa.eu/press/pr/date/2020/html/ssm.pr200320~4cdbbcf466.en.html

European Central Bank, 2020b, Letter. April 1. https://www.bankingsupervision.europa.eu/press/letterstobanks/shared/pdf/2020/ssm.2020_letter_on_Contingency_preparedness_in_the_context_of_COVID-19.en.pdf?d1c8dc2780e2055243778bedf818efeb

Fernández de Lis, S., Martínez, J., Saurina, J., 2000. Credit growth, problem loans and credit risk provisioning in Spain. Working PaperN. 0018, Banco de España.

Financial Stability Board (2009), Report of the financial stability board to G20 leaders, secretariat based in Basel, Switzerland.

Fonseca, A.R., Gonzàlez, F., 2008. Cross-country determinants of bank income smoothing by managing loan-loss provisions, Journal of Banking and Finance, 32, 217-228.

Fudenberg, D., Tirole, J., 1995. A theory of income and dividend smoothing based on incumbency rents. Journal of Political Economy 103 (1), 75-93.

G20 (2009), Declaration on Strengthening the Financial System, April 2nd, London.

Goel, A.M., Thakor, A.V., 2003. Why do firms smooth income? Journal of Business 76(1), 151-192.

Greenwalt, M., J. Sinkey, Jr., 1988. Bank loan loss provisions and the income smoothing hypothesis: An empirical analysis. Journal of Financial Services Research Vol. 1, pp. 301-318.

Hasan, I., Wall, L., 2004. Determinants of the loan loss allowance: some cross-country comparison, The Financial Review, Vol. 39 pp.129-152.

Hicks, J. 1980. Causality in Economics. Blackwell. Oxford.

IMF, 2020a, World Economic Outlook April 2020, https://www.imf.org/~/media/Files/Publications/WEO/2020/April/English/text.ashx?la=en.

IMF, 2020b, World Economic Outlook Update June 2020, https://www.imf.org/~/media/Files/Publications/WEO/2020/Update/June/English/WEOENG202006.ashx?la=en.

Kanagaretnam, K., Lobo, G.J., Yang D.H., 2005. Determinants of signaling by banks through loan loss provisions. Journal of Business Research 58, pp. 312-320.

Kim, M., Kross, W., 1998. The impact of the 1989 change in bank capital standards on loan loss provisions and loan write-offs. Journal of Accounting and Economics Vol. 25(1), pp. 69-100.

Laeven, L., Majnoni, G., 2003. Loan-loss provisioning and economic slowdowns: too much, too late? Journal of Financial Intermediation, Elsevier, vol. 12(2), pp. 178-197, April.

Leuz, Ch., Nanda, D., Wysocki, P., 2003. Earnings management and investor protection: An international comparison. Journal of Financial Economics 69, pp.505-527.

Liu, C., Ryan, S., 1995. The effect of bank loan portfolio composition on the market reaction to and anticipation of loan loss provisions. Journal of Accounting Research Vol. 33(1) pp. 77-94.

Liu, C., Ryan, S., Wahlen, J., 1997. Differential valuation implications of loan loss provisions across banks and fiscal agents. The Accounting Review Vol. 72(1) pp. 133-146.

Lobo G.J., Yang, D.H., 2001. Bank Managers’ Heterogeneous Decisions on Discretionary Loan Loss Provisions. Review of Quantitative Finance and Accounting, Vol. 16, pp. 223-250.

Ma, C.K., 1988. Loan loss reserve and income smoothing: The experience in the U.S. banking industry. Journal of Business Finance and Accounting, Vol. 15, No. 4 pp. 487-497.

Masera R., 2019. Community Banks and Local Banks. ECRA, Roma.

Masera R., 2020. Leverage and risk weighted capital in banking regulation, IUP Journal of Bank Management. February, pp.7-57.

Moyer, S.E., 1990. Capital adequacy ratio regulations and accounting choices in commercial banks. Journal of Accounting and Economics, 13 (July): pp. 123-154.

Ng, J., Roychowdhury, S., 2011. Do Loan Loss Reserves Behave like Capital? Evidence from Recent Bank Failures. Available at SSRN: http://ssrn.com/abstract=1646928

Nichols, D., Wahlen, J., Wieland, M., 2009. Publicly-traded versus privately-held: implications for conditional conservatism in bank accounting. Review of Accounting Studies, 14, 88-122.

Perez, D., Salas, V., Saurina, J., 2006. Earnings and capital management in alternative loan loss provision regulatory regimes. Banco de España Working Paper, n°614.

Pesola, J., 2011. Joint effect of financial fragility and macroeconomic shocks on bank loan losses: Evidence from Europe. Journal of Banking and Finance, 35, pp.3134-3144.

Peters, O., 2019. The ergodicity problem in economics. Nature Physics, pp.1216-1221.

Petropoulou, A. et al., 2020. The efficiency of Us community banks. SSRN. https://papers.ssrn.com/sol3/Delivery.cfm/SSRN_ID3550458_code2988435.pdf?abstractid=3550458&mirid=1

Ronen J., Sadan, S., 1981. Smoothing income numbers: objectives, means and implications. Addison-Wesley Publishing Company.

Scheiner, J.H., 1981. Income smoothing: an analysis in the banking industry. Journal of Bank Research 12, 119-123.

Scholes, M., Wilson, G.P., Wolfson, M., 1990. Tax planning, regulatory capital planning, and financial reporting strategy for commercial banks. Review of financial studies Vol. 3 pp. 625-650.

Trueman, B., Titman, B., 1988. An explanation of accounting income smoothing. Journal of Accounting Research 26 (supplement), 127-139.

Tsay, R. S.,2010. Analysis of Financial Time Series. Wiley. London.

Wahlen, J., 1994. The nature of information in commercial bank loan loss disclosures. The Accounting Review Vol. 69(3) pp. 455-478.

Wetmore, J.L., Brick, J.R., 1994. Loan loss provisions of commercial banks and adequate disclosure: a note. Journal of Economics and Business 46, 299-305.

Zamil, R., 2020, Expected loss provisioning under a global pandemic. FSI Briefs, 2.

Authors

Rosa Cocozza is Full Professor of Banking and Finance at the Università degli Studi di Napoli Federico II, Department of Economics, Management, Institutions, rosa.cocozza@unina.it, https://www.docenti.unina.it/rosa.cocozza.

Rainer S. Masera in Professor of Political Economy and Dean of the Economics Faculty at the Università Guglielmo Marconi, r.masera@unimarconi.it, https://www.unimarconi.it/en/rainer-masera.

[1] The impact of IFRS 9 on the procyclicality of loan loss provisioning is ambiguous. Provisioning for a next economic downturn under the expected credit loss model may be rather abrupt, if an initial turning point in the business cycle is taken to forebode a serious business cycle downturn, triggering large loan loss provisioning in anticipation of future loan impairment. The introduction of the expected credit loss model thus could lead to a concentration of loan loss allowances at the time of an initial economic downturn, with possible negative ramifications for financial stability. Simulations by Abad and Suarez (2017) confirm this by showing that IFRS 9 will concentrate the impact of loan loss allowances on profitability and the CET1 ratio at the beginning of the economic cycle, yielding that banks will face a higher yearly probability of having to be recapitalised.

[2] The list of banks used for Supervisory Banking Statistics comprises banks designated as significant institutions (SIs) and thus directly supervised by the European Central Bank (ECB). Size-based classification (expressed in terms of total assets) is linked to the bank systemic importance and risk-taking. Dataset classification thresholds are defined in such a way as to foster comparability with the existing SSM and European Banking Authority (EBA) practices, distinguishing between global systemically important banks (G-SIBs; as listed by the Financial Stability Board (FSB)), large banks, medium-sized banks (two subcategories) and small banks. The EBA has defined an asset threshold of €200 billion for the identification of large institutions that are potentially systemically relevant. Moreover, since one criterion for identifying banks as “significant” under SSM regulations is that their total assets should exceed €30 billion; this threshold has been used to distinguish “small banks” which enter the SI list via the other criteria. Finally, medium-sized institutions include all those that fall between small and large and are clustered in two buckets separated by a €100 billion threshold.

[3] Nevertheless, it is noteworthy that income-based measures could overestimate the degree to which some credit institutions are engaged in non-credit activities since loans can generate both interest and noninterest income in terms of fees; therefore asset-based measures are more useful for distinguishing between activity categories (Ciocchetta, 2020).

[4] The classification of a loan as an NPL is “objective evidence that the loan should be assessed for impairment”.

[5] The point at issue is that macroprudential and microprudential approaches can lead to different conclusions. The expected loss approach can itself lead to procyclicality in case of extremely adverse economic developments: excessive tightening of credit with further adverse economic consequences. The need for extraordinary fiscal and monetary support measures was predicated precisely because indebted firms may not suffer a fundamental deterioration in the lifetime probability of default. The complex two-way relationship has been recognized by the ECB itself, 2020a and 2020b.

[6] The bank data used in this paper for the estimates are constrained by the availability of information on some variables needed for this research.

You must be logged in to post a comment.